Nov. 15, 2012 | CREBNow

Track Spending Today, Save for the Future

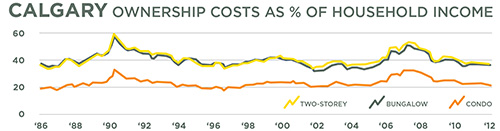

The BMO Financial Group is offering some tips to maintain a balanced household budget.Keeping the household books balanced is one of the most common challenges Canadians face these days in achieving their financial goals. According to Statistics Canada, Canada's personal savings rate peaked in 1982 at 20 per cent and since then has decreased to about five per cent and the household debt-to-income ratio is currently 152 per cent, a record high.

BMO stated the combination can make it difficult to balance the books, especially since many Canadians are balancing pay o debt while saving for their future. As well, the summer months can create more of a challenge due to vacations and busier social calendars.

"It can be easy to lose track of daily expenditures, especially during the busy summer months, which may result in unwelcome surprises at the end of the month that can derail the household balance sheet," said Andrew Irvine, senior vice president, BMO. "The first step to finding a balance between paying down debt and saving for big picture goals, however, is getting day-to-day spending under control."

Tips the bank offered include focusing on where you can scale back, say, your morning co ee; staying current with new costs that can appear at any time; setting and sticking to financial goals and finding the balance between saving while paying o ff debt.

What are some of your money saving tips? Share in the comments below.

Tagged: Calgary Real Estate | Calgary Real Estate News | Home Owners

Related Articles

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}