Oct. 25, 2017 | Mario Toneguzzi

The bigger picture

Thinking long-term puts Calgary's housing market in perspective

Thinking long-term puts Calgary's housing market in perspectiveReal estate is a numbers game, and looking at those numbers over an extended period truly does shine a light on the performance of a market over the long-term.

From that perspective, home prices in Calgary have been very impressive.

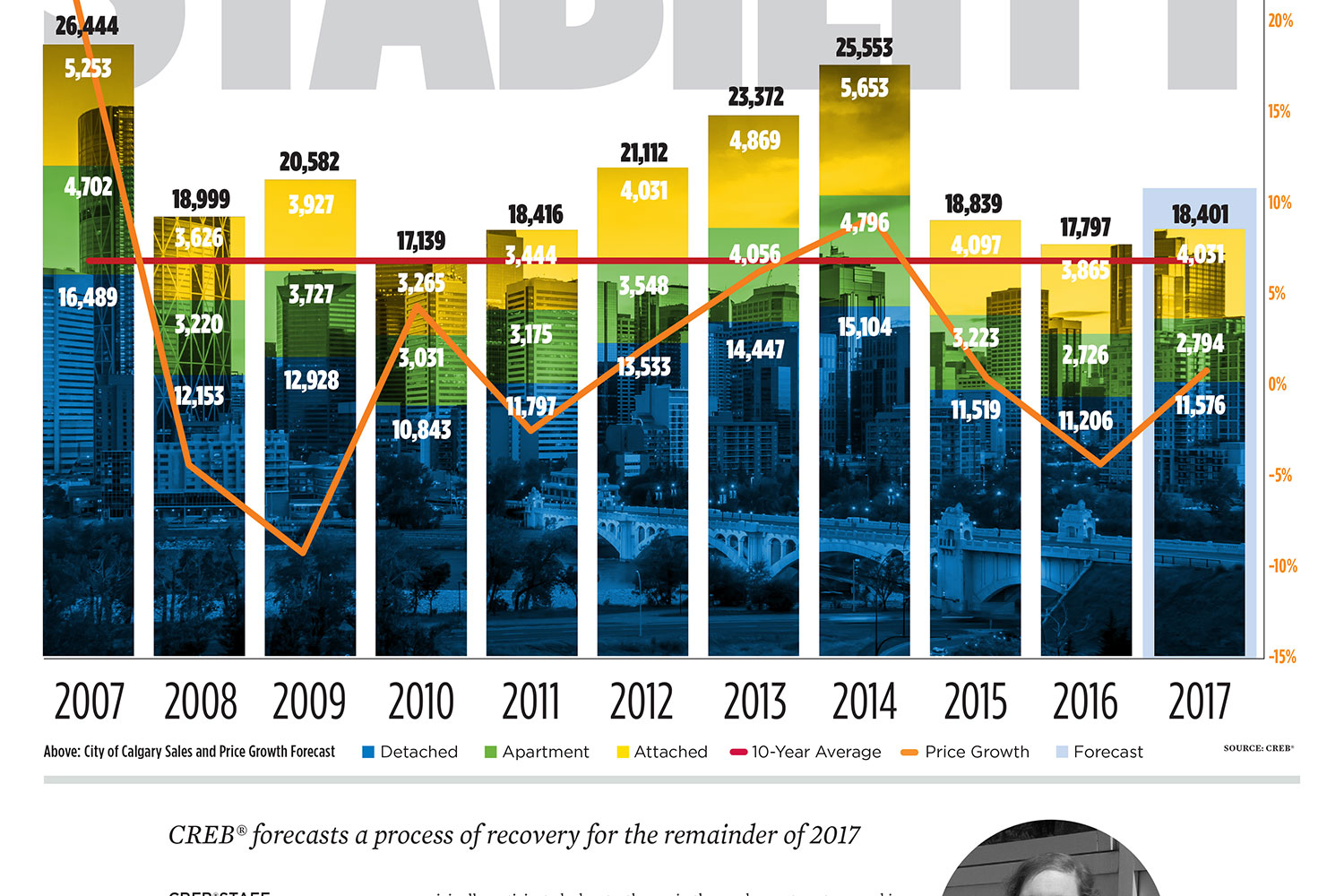

Here is something to consider. The MLS® System benchmark price in 2004 was $213,267, which jumped to $231,567 in 2005, $335,517 in 2006 and finally $410,717 in 2007. Over the past decade, those prices have fluctuated in response to the strength of Calgary's economy. In 2016, the annual benchmark price was $438,567 and this year, up to the end of September, it was $438,322.

"Generally, we do see a level of appreciation," said Ann-Marie Lurie, CREB® chief economist. "If you look at the growth following that period (from 2005 to 2007) . . . you're seeing a level of appreciation that's fairly slow but steady.

"Granted, we've had two corrections since then, so we have to keep that part in mind. But when you look at it on a longer-term basis, it really is a very slow, moderate appreciation on annual prices. So, housing prices generally have been improving."

She says it's important for people to consider how long they intend to be in their purchased home, since housing is really a long-term asset.

"There are periods when many Calgarians considered average price increases of double digits, year after year, to be the norm, so when the market slows, flattens and corrects to normal conditions it feels like the world is ending. Higher highs bring lower perceived lows." - Don Campbell Real Estate Investment Network senior analyst

Don Campbell, senior analyst with the Real Estate Investment Network, says Calgary has historically had one of the most volatile average home price statistics in the country.

"This has made it a market that has never been good for the faint of heart," said Campbell.

"While cities in other provinces are buffered and protected by additional factors, the Calgary region has become almost the perfect case study of the impact of economics and demographics on a housing market. GDP grows, followed by job growth, which attracts new residents, which drives housing demand of multiple types. Then, when the oil and gas economy takes its inevitable pause, the reverse occurs and becomes very apparent in housing stats. We do not witness that quick of a correlation in many other major centres in Canada."

Although headlines and commentary often focus on snapshots in time in housing markets, Campbell says strategic investors and homeowners understand that in Calgary, it's a long-term outlook that helps weather the inevitable economic storms.

"Average incomes in Alberta as a whole, and Calgary specifically, are higher than the rest of the country, and thus, when things are good, that higher income drives move-ups and homeownership rates up more quickly than is normally experienced in other cities," he said.

"On the upswing, rents and values often overshoot, and then, when the downturn occurs, the drop can be read as quite dramatic. There are periods when many Calgarians considered average price increases of double digits, year after year, to be the norm, so when the market slows, flattens and corrects to normal conditions it feels like the world is ending. Higher highs bring lower perceived lows. However, when one views that actual net increase over 10-year periods, the average doesn't look as bad as those snapshots in time."

Tagged: Ann-Marie Lurie | Calgary Real Estate News | CREB® Chief Economist Ann-Marie Lurie | Don Campbell | Guest Column | Housing Market | Housing Market | Mario Toneguzzi | MLS | MLS® System | real estate investment network | REIN

Related Articles

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}