April 21, 2021 | CREBNow

Housing Market – Row

Sales in the first quarter totalled just under 800 units, making it the strongest first quarter for sales since 2007.However, new listings also rose to relatively high levels. The pace of sales growth outpaced the growth in new listings, slowing the typical quarterly gains in inventories and causing inventories to ease relative to last year. Despite the year-over-year declines, inventories remain elevated relative to the levels recorded prior to the economic downturn caused by the energy sector back in 2014.

Strong sales growth and easing inventory levels caused the months of supply to trend down to three months, the lowest level seen in over five years. The months of supply for this sector has been trending down over the past several quarters, but it was only in the past two quarters that levels were either consistent with or below longer-term trends.

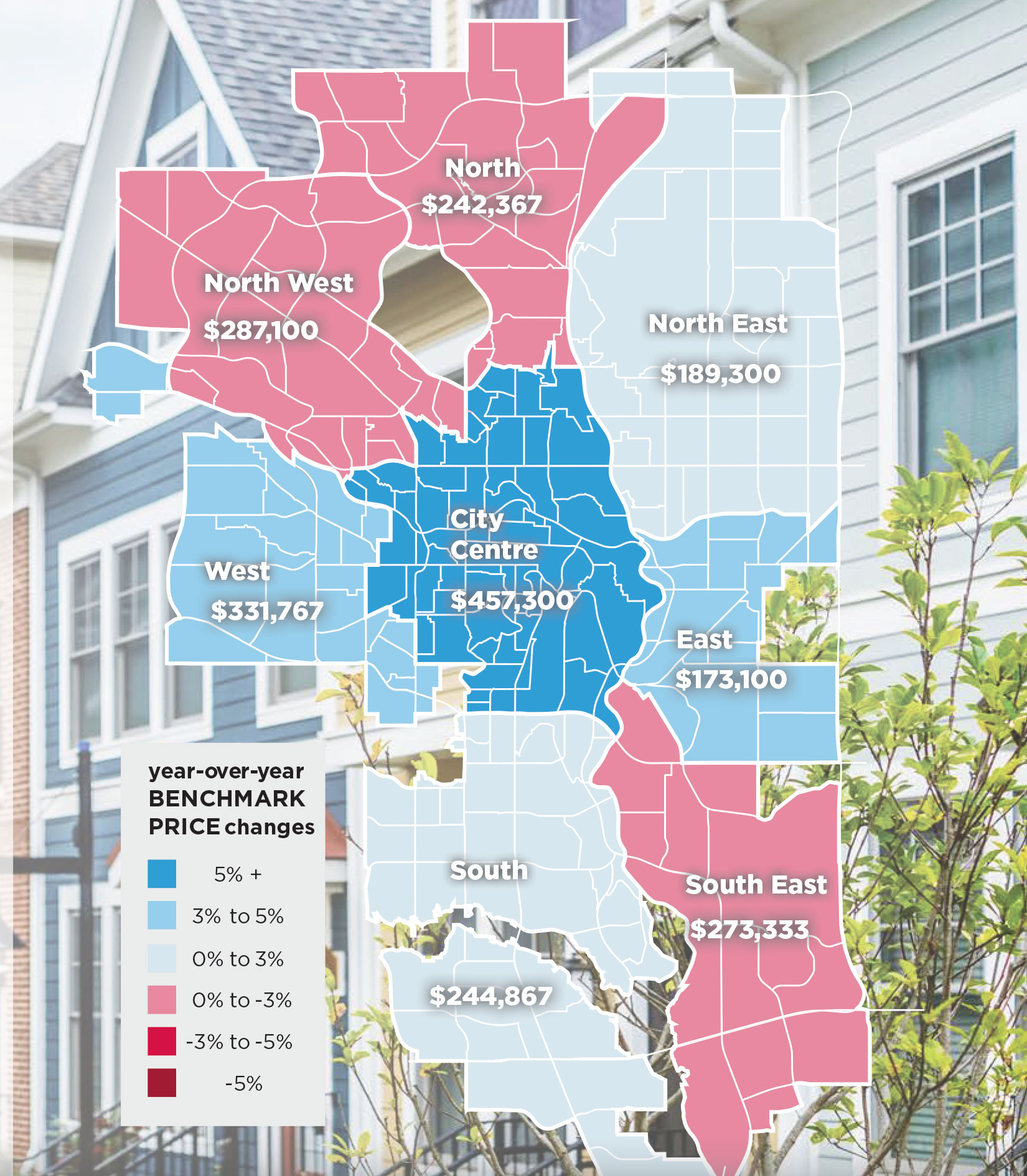

As this segment of the market is generally more balanced relative to the detached sector, price gains have stayed at moderate levels. Prices have been trending up over the past three quarters and now sit over one per cent higher than prices from the first quarter of 2020.

As this segment of the market is generally more balanced relative to the detached sector, price gains have stayed at moderate levels. Prices have been trending up over the past three quarters and now sit over one per cent higher than prices from the first quarter of 2020.However, price movements have varied across each district. The most significant year-over-year gain occurred in the City Centre at over six per cent, pushing this district much closer to price recovery.

Prices remained lower than last year's levels in the North, North West and South East districts. This could be related to competition from new builds in those areas, placing some limits on resale prices.

Click here to download the full Q1 2021 Housing Report

Tagged: Calgary | Calgary Real Estate | Calgary Real Estate News | Q1 Report 2021

Related Articles

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}