Aug. 10, 2016 | Jamie Zachary

Moving forward

CREB®'s mid-year update cites tough start to 2016, forecasts continued challenges moving forwardCalgary's housing market will continue to battle recessionary conditions during the second half of 2016, but the worse might be behind it.

That's the word from CREB® as it released a mid-year update to its annual Economic Outlook & Regional Housing Market Forecast.

"With no near-term changes expected in the economic climate, housing demand is expected to remain weak for the second consecutive year as resale activity is forecasted to decline by eight per cent in 2016," said CREB® chief economist Ann-Marie Lurie, who authored the report.

"However, indicators do reflect some easing of the supply pressure in the market, which should limit some of the downward pressure on prices this year."

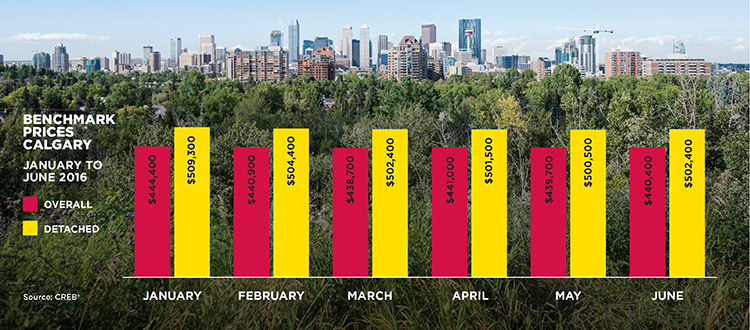

CREB® revised its forecast on citywide annual prices to drop by 3.8 per cent to $440,812 by the end of 2016. That's compared with the 3.4 per cent decline the REALTOR® organization originally expected at the start of the year.

Lurie cited ongoing uncertainty within the energy sector behind the housing market's continued downturn. While spring WTI prices hovered near $50 US per barrel, prices since then have adjusted to a lower level as excess supply continues to impact oil markets. She pointed to current forecasts pegging WTI prices around $43 this year and $52 in 2017.

"More volatility with oil prices that are already low, combined with political uncertainty, is expected to cause further contraction in investment activity and ultimately impact future employment potential," she said.

While Lurie acknowledged Calgary's current economy is still not as dire as the 1980s when considering migration, unemployment and lending rates, she noted job levels have still contracted more than expected in the first half of the year, and fewer people have moved into the province for work. According to the recent City of Calgary census, net migration went from 24,900 in April 2015 to a net outflow of 6,527 people – a 31,427 change in the number of net migrants. The last time the outflow of migrants surpassed the inflow was in 2009.

"Current indicators have been revised down to reflect a much deeper and longer recession."

"Current indicators have been revised down to reflect a much deeper and longer recession, potentially extending periods of time where people are out of work and making it more difficult to find employment at a comparable salary," said Lurie, noting that so long as the energy sector underperforms, Calgary's housing market will continue to face headwinds – even sometime after energy prices stabilize at more optimal levels.

"When oil prices improve, it may take some time to see this translate into job and wage growth in the province. With over 30,000 full-time jobs lost, many of those people will need to get back to work before the housing market starts to stabilize. This would require several months of full-time job creation and a reduction in the unemployment rate, translating into demand growth and greater absorption of additional supply in the market.

"Based on current expectations, it is possible to see more housing market volatility by the end of the year with some house price stability as we move into 2017.

Resale

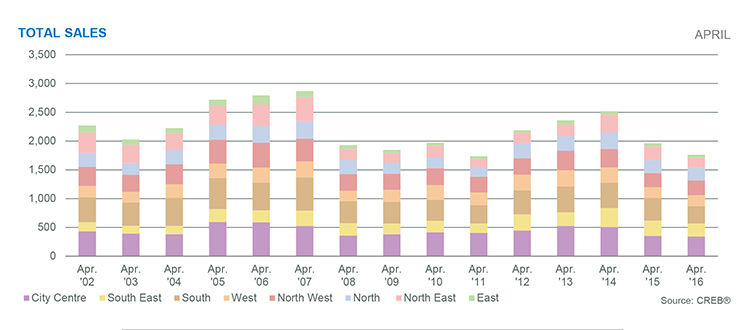

Sales activity on the MLS® System outpaced original estimates during the first six months of 2016, declining by 10 per cent to 9,205 units, noted CREB®. Its original forecast, called for a 2.2 per cent drop in transaction levels.

Looking forward to the second half of 2016, CREB® predicted sales activity in the city will continue its downward momentum, albeit not as steep, to eight per cent by year's end, or 17,321 units. It originally forecasted 18,416 transactions in 2016.

Despite double-digit sales declines over the first two quarters, benchmark prices did not experienced a free fall – a fact Lurie attributed to inventories that, while steadily rising, have remained well below historical highs.

Year-to-date new listings totaled 21,191 units, a two per cent decline over the previous year, and 11 per cent below the 10-year average. That's also 32 per cent below the same period where record highs were recorded in 2008 at 31,049 units.

"Given slower demand, the decline in new listings helped prevent inventory levels from reaching the highs recorded in 2008," said Lurie, adding, "The situation could be worse."

"With so much choice out there, it's giving consumers an opportunity to find their ideal home at a price they can afford."

Lurie also noted supply gains have been tempered by factors such as savings, severance packages and unemployment insurance, "all of which helped buy time for those who have lost their jobs. If the same conditions persist into 2017, we could potentially see more supply pressure from those in a must sell scenario, further impacting housing prices."

While not good for sellers, CREB® president Cliff Stevenson noted some buyers have benefitted from price declines so far in 2016, allowing them to get into homes that were previously unattainable.

"This is especially true for homeowners with financial stability and a good amount of equity in their home," he said. "With so much choice out there, it's giving consumers an opportunity to find their ideal home at a price they can afford."

Investors have also had an opportunity to benefit from a downturn in demand, noted Don Campbell, a senior analyst with the Real Estate Investment Network. Those who may not have been able to acquire income-generating apartment properties a year ago are now able to get them at a discount.

"The upsides are simply that the patient investors will have a chance over the next six to 12 months to find good solid deals in good solid buildings from people who had bought on speculation or who are less experienced at managing rentals in a slower market," he said.

Differences among sectors

Not all sectors of Calgary's housing market will be impacted the same during the rest of 2016. CREB® forecasted the steepest sales and price declines will continue to exist in the apartment and row sectors, of the market, with some leveling in the detached and semi-detached markets by the end of the year.

The apartment sector will likely fare the worst due to increased competition from rental product, new construction and resale housing. CREB® updated its forecast on apartment sales activity, which accounts for approximately 20 per cent of the market, to fall by 19 per cent from last year's levels to 2,515 units. It originally called for a two per cent drop to 3,163 transactions.

With supply far outpacing demand ... further price declines are anticipated."

While inventories in the first two quarters did not reach the same highs recorded in 2008, they averaged 1,496 units so far this year, 15 per cent above last year's levels and 21 per cent above long-term averages.

"With supply far outpacing demand ... further price declines are anticipated until the additional supply from all other sources in the market can be absorbed," said Lurie, pointing to an expected 5.6 per cent annual decline in the apartment benchmark price by year's end. "Until those inventory levels decrease, it's anticipated that this sector of the market will continue to face the most challenges.

The attached sector, meanwhile, saw sales declines primarily in row-style product versus semi-detached. While inventories expanded in both sub-sections, the rise was far more significant for row product, which resulted in a greater imbalance between supply and demand levels and, ultimately, larger price declines.

Moving forward, CREB® forecasted attached sales overall to decline by eight per cent to 3,763 units by year's end. CREB® originally forecasted a 1.5 per cent drop. The attached benchmark price is also expected to fall by 4.2 per cent on an annual basis, yet CREB® noted they will remain above 2008/09 levels.

The detached sector, which accounts for more than 60 per cent of Calgary sales, will fare better than others moving forward. However, certain price segments will react differently, noted Lurie.

Challenges that were once isolated in the higher price range will continue to spread to other areas of the market, creating price adjustments in virtually all areas of the city.

"Supply and demand imbalances will likely ease in this segment and limit some of the downward pressure on aggregate detached prices, noted Lurie, who forecasted price declines to average 3.2 per cent for the year, while sales to fall by five per cent.

A drop in new listings, combined with less competition from standing inventory in the new home sector, will likely further mitigate significant price declines in the detached sector moving forward, she added.

Tagged: Apartment | attached | benchmark price | Calgary Real Estate | Calgary Real Estate News | City of Calgary | CREB® Chief Economist Ann-Marie Lurie | CREB® president Cliff Stevenson | detached | Don Campbell | forecast | Housing Market | Housing Market | inventory | mid-year forecast | months of supply | net migration | new listings | Oil Prices | Population | sales | unemployment | YYCRE

Related Articles

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}