Jan. 12, 2016 | Alex Frazer Harrison

Here we go again

Comparing Calgary's current downturn to historyCalgary's infamous boom-bust economy is at it once again.

Just as it did in the 1980s and late-2000s, economic conditions have once again turned sour.

But does this downturn feel different from those that came before?

Yes, says CREB® chief economist Ann-Marie Lurie.

In CREB®'s 2016 Economic Outlook & Regional Housing Market Forecast, Lurie notes that while some have tried to compare this year to the early 1980s – in terms of its perfect storm of low oil prices and high unemployment – the underlying conditions are, in fact, much different.

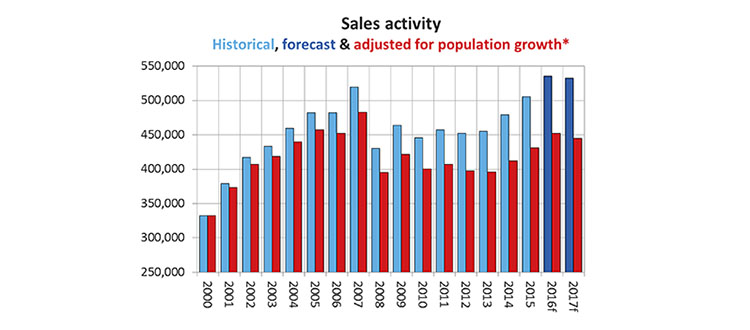

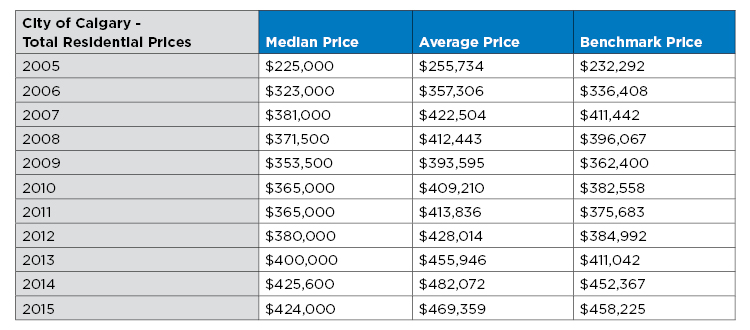

Between 1981 and 1985, average annual home prices plunged 20 per cent, with 20 per cent also the average five-year term lending rate. But Lurie forecasts a "less severe pullback" in home prices this time, with positive (if slowing) net migration also a mitigating factor, plus housing supply levels 35 per cent lower than they were in 2008 and interest rates at historic lows.

"For Calgary to see price drops comparable to the 1980s, the current economic downturn will have to last for an extended period of time," said Lurie in the forecast.

Conference Board of Canada deputy chief economist Pedro Antunes, meanwhile, dismisses comparisons with the downturn in 2008/09. For one, this one is localized, he noted.

"The rest of the world isn't feeling the same, and we don't have a financial crisis (like 2008)," he said. "We don't have a situation where there's a complete drying up of access to capital."

Allan Dwyer, assistant professor of Finance at Mount Royal University's Bissett School of Business, believes the current downturn has similarities to others, including the one that gripped Montreal following the election of a Bloc Quebecois government in 1976, the Japanese stock market collapse of 1989 and ongoing issues in Detroit that climaxed with that city declaring bankruptcy in 2013.

Although the circumstances are different, all of these downturns share common elements, noted Dwyer:

• A sense of uncertainty still exists about Alberta's first non-PC government in decades;

• Calgary – like Japan – went through a long period of "feeling of wealth" before circumstances changed; and

• The changes in automobile manufacturing that impacted Detroit could be compared to how new technologies in oil production – meaning "the way we produce the bulk of our oil is basically a dinosaur."

For Alberta to get out of its current slump – something it took Montreal 15 years to recover, and arguably, Japan has yet to do so fully – Dwyer said the province must "adjust or adapt."

"The Calgary market, the real estate market, employment levels – so (much) is tied to that idea of oilsands oil," he said.

"We have to move toward this business of 'tight oil' and new type of technologies. We have to think about how we do oil and gas and energy. Is it just hydrocarbons? Or is it solar, renewables, tight oil, fracking ... a whole portfolio of energy production so we maintain ourselves as an energy exporter, but not dependent on very expensive oilsands production."

Antunes said if oil prices remain flat, he anticipates a "flat economy" for Alberta in 2016, with the Conference Board anticipating a 1.2-per cent provincial contraction in 2015.

"We do think that oil prices will come up to the $65-70 range over the medium term, which should make the industry return to profit or at least viability," said Antunes.

Tagged: Calgary Real Estate News | CREB® Chief Economist Ann-Marie Lurie | downturn | Economy | Energy | forecast | Housing Prices | Mount Royal University | Oil Prices | recession | YYCRE

Related Articles

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}