March 26, 2014 | CREBNow

Bubble Fears 'Exaggerated'

According to a new report from the Conference Board of Canada, any fears of a housing bubble in the country are "exaggerated".The report, Housing Briefing: Bubble Fears Overblown takes a look at Canadian home prices which might be headed for a decline across the country, but eases any fears of a housing bubble. "Mortgage costs, not just house prices, are the principal deciding factor for potential homebuyers," said Robin Wiebe, senior economist, Centre for Municipal Studies. "Mortgage rates are expected to rise this year, but not dramatically, because the Canadian economy remains in slow-growth mode."

The Conference Board of Canada said fears of a housing bubble hinge on the ratio of house prices to apartment rents and house prices to incomes. The board's view is that while these ratios are high they may also be misleading. An improvement on looking at affordability is the ratio of mortgage payments to rents and mortgage payments to incomes while neither show much cause for any housing bubble alarms.

Other factors pointing away from a potential housing bubble are the combined growth of both Canadian employment and population. For the most part housing starts are in line with demographic requirements and the board said markets do "not appear to be overbuilt." Total housing starts in Canadian cities with at least 10,000 residents ended 2013 at just below 170,000 units. While that's down from nearly 194,000 starts in 2012, the Conference Board said it's in line with Canada's 25-year average.

As far as home sales, the Canadian Real Estate Association (CREA) reported home sales are expected to trend higher as spring progresses to be further supported over the second half of 2014 with an "anticipated" increase in economic growth.

"I expect fixed mortgage rates will edge marginally higher in the second half of 2014 as evidence confirms an anticipated pick-up in economic growth," said Gregory Klump, CREA's chief economist. "Marginally higher mortgage rates are likely to counterbalance the lift provided by stronger economic and continuing job growth, and restrain the momentum for sales activity."

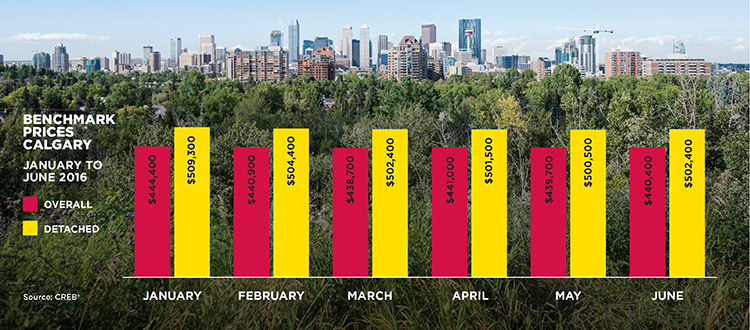

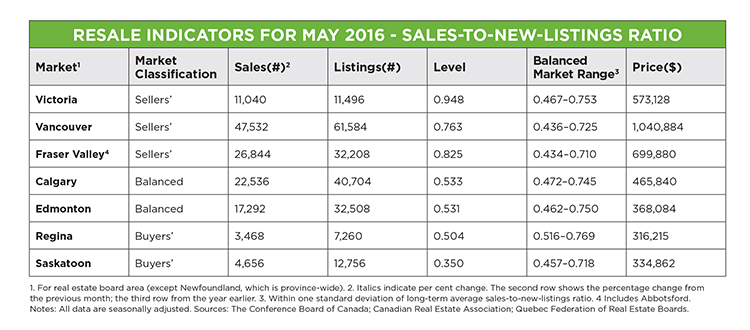

The Conference Board of Canada report assessed six major Canadian markets including Calgary. They said the local resale market is approaching "sellers conditions" with sales not falling on a year-over-year basis since April 2011 and price growth "accelerated sharply" in 2013. Last month in Calgary saw an 8.68 per cent increase in sales over the same period in 2013 at 1,854 units. While slower sales growth resulted in fewer listings in the single-family sector, sales in that sector still increased 1.9 per cent when compared to February 2013.

In Vancouver the Conference Board said the resale market has moved back into balance and sales were up from a year earlier; Edmonton is seeing price growth increase along with sales; Toronto's sales stabilized in June of last year and a decrease in employment is contributing to slowing resale conditions in Ottawa.

Tagged: Calgary Real Estate | Calgary Real Estate News | Conference Board of Canada

Related Articles

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}