Aug. 09, 2012 | Cody Stuart

Bigger, Better, Sooner

When it comes to purchasing a first home, buyers have regrets – mostly that they took so long to do it.In that sense, Bryan Backman- Beharry is your typical homebuyer. The 32-year-old Calgarian recently purchased his first home, a three-bedroom bungalow in the southwest community of Killarney, after renting a condominium in the downtown core. "I tend to be very cautious about major purchases, so I feel that I did sufficient due diligence and bought at a time that made financial sense for me," he said. "I suppose my only regret is that I did not buy a house 10 years ago when they were much less expensive."

Judging by the findings of a new report from TD Canada Trust, Backman-Beharry is far from alone in his sentiments. According to the 2012 TD Canada Trust First Time Home Buyers Report, the top three lessons learned from new homebuyers included making a bigger down payment (60%), budgeting better (60%) and buying sooner (55%).

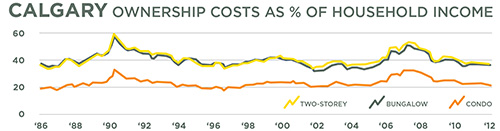

According to Royal LePage, the average house price in Calgary has increased from $189,500 in 2002 to $429,000 in 2012.

The top reasons home buyers give for deciding when to buy their first home is they tire of paying rent (48%), get a full time job (31%) or want to start a family and need more space (31%). Many first time buyers say if they could do it again, they would have bought sooner (55%), however 60 per cent also say they wish they would have made a bigger down payment (likely requiring more time to save).

"After having rented a condo downtown, I decided it made more financial sense to be putting that money toward a mortgage and have something to show for it down the line," said Backman- Beharry. "The Calgary housing market seems to be strong and improving every year, so I consider it a fairly safe investment."

Like Backman-Beharry, the majority of first time buyers in the TD report said they were looking for a detached home (54%), with condos coming in a distant second (18%).

In Edmonton on a January to July basis, Hirsch said single-family dwellings are higher by two per cent over the same seven month period last year.

The mortgage rule changes announced by the CMHC included reducing the amortization period from 30 to 25 years and decreasing the amount Canadians can borrow when financing a home from 85 to 80 per cent of the value.

However, the stability seen in Alberta isn't the same across the country. In Vancouver and Toronto home prices have started to show signs of decreasing. Hirsch said according to the Vancouver Real Estate Board sales activity in July decreased by 11.2 per cent compared to June.

"Alberta's stronger economy, better job prospects and higher wages, have contributed to the healthy real estate market," said Hirsch. "Still the CMHC change has had an impact. The shorter amortization period has without question removed some potential buyers from the market and forced other buyers to consider less expensive homes."

Are you a new home owner? What have you learned from the process of purchasing your first home? Any advice you would give to other purchasing their first home? Share your experience in the comments below.

Tagged: Calgary Real Estate | Calgary Real Estate News | Home Buyers

Related Articles

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}