July 18, 2016 | Jamie Zachary

A return to balanced

Indicators suggests Calgary's housing market might be evening outNew housing market statistics are reinforcing the emergence of so-called balanced conditions in Calgary.

In its monthly stats package for June, CREB® noted key segments of the local market are seeing increased price stabilization brought upon by more moderate sales declines and listing increases.

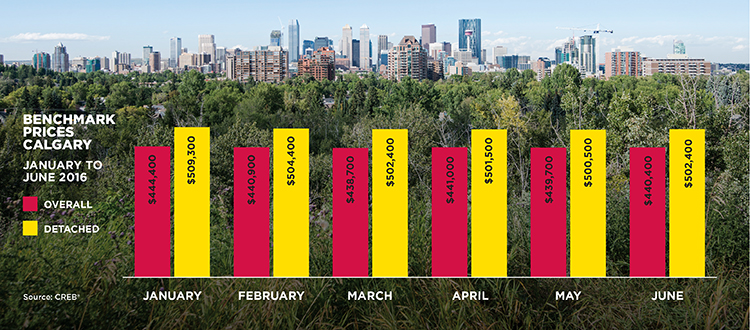

CREB® chief economist Ann-Marie Lurie singled out last month's detached sector, which saw new listings decline at a faster rate than sales (five and 3.7 per cent, respectively) for only the second time in the past 12 months – the last time coming in January. As a result, the sector's benchmark price totaled $502,400, which was 0.4 per cent higher than May, yet still 3.4 per cent lower than last year's levels.

The detached market represents nearly two out of every three sales in the city.

"The detached market has been gradually moving toward more balanced conditions, helping to prevent price levels from declining at the faster rates we saw in the previous two quarters," said Lurie, noting months of the supply in the sector has been below three since March. Months of supply, regarded by Lurie as an indicator of balanced conditions, is the amount of time it would take to sell current inventory.

"It's a moment-in-time snapshot, but the detached market has been gradually moving toward more balanced conditions."

"While this is welcomed news for sellers, it's very likely that pricing challenges will persist in the housing market until economic conditions start to improve."

June represented the first time in eight months that detached prices recorded a monthly gain, helping ease the quarterly decline from 2.2 per cent in the first quarter to 0.7 per cent in the second quarter, noted CREB®.

"It's a moment-in-time snapshot, but the detached market has been gradually moving toward more balanced conditions," said CREB® president Cliff Stevenson.

"This is an interesting dynamic in a market that continues to see sliding home prices in all other segments. It also validates the message that consumers need to discuss what is currently happening in the real estate market with a real estate professional, so they know how it could affect their ability to buy or sell in a particular neighbourhood, community or district."

Overall, Calgary's benchmark price in June was $440,400, even with May yet a 4.1 per cent drop from the same time last year. CREB® attributed price softness to ongoing challenges in the apartment and, to a degree, attached markets.

CREB®'s report is the second reference to balanced conditions in as many weeks. Late last month, Conference Board of Canada economist Robin Wiebe classified Calgary's overall housing market in May as balanced, noting sales volumes increased by 1.6 per cent on a month-over-month basis, while listings declined by 1.9 per cent.

Wiebe noted the city's sales-to-new listings ratio in May sat at 0.533. The city's balanced range is 0.472 to 0.745.

Looking ahead, Wiebe anticipates the city's MLS® price will increase between zero and 2.9 per cent over the short term.

The fact that Calgary housing prices have not experienced a free fall, even though the price of oil has, should not be a surprise, said ATB Financial chief economist Todd Hirsh. For one, we continue to see historically low interest rates.

"In 2016, an average mortgage is three to three-and-a-half per cent," he said. "Even if you have one income in the household still operating, you're at least more likely to make the minimum payment and avoid default. That means you are not going to be forced to liquidate your house, which then means there's not as much product flooding onto the market as we would have seen in previous years.

"What we saw in the 1980s – (as well as) in places like Las Vegas and Phoenix six years ago — was a tidal wave of mortgage foreclosures hitting the market at the same time. That's really what you need to see to drive prices down 20 or 25 per cent. And that's what we saw in Calgary here in the 1980s – where there was a tidal wave of foreclosures."

"For me, I wouldn't use the word crash until the housing prices were down by more than 20 per cent year-over-year or maybe from the peak."

Hirsch noted another difference is Alberta has proportionately more two-income homes. In 1976, 46 per cent of Albertans were two-income households, compared with 64 per cent now, according to Statistics Canada.

While Hirsch admits to hearing whispers of "crash" when describing Calgary's housing market, he said the evidence doesn't support it.

"For me, I wouldn't use the word crash until the housing prices were down by more than 20 per cent year-over-year or maybe from the peak," he said. "Right now, by the time everything is said and done in Calgary, we'll be looking at probably a five per cent or seven per cent (decline) – maybe. That's noticeable, especially if you're the seller, but I think the word 'crash' or 'collapse' is a bit overdone when something falls five or seven per cent."

Lurie added it is rare for a market to experience a collapse in housing prices over a quick period of time. Part of that is because housing tends to be the last thing affected by an economic downturn – and by that time, economic conditions tend to level out or improve.

She admitted what constitutes a crash in the market will always be subjective, with different pundits having different opinions.

"When they're using the word crash to me that's a sensational term anyway," said Lurie.

- With files from Mario Toneguzzi

Tagged: Apartment | ATB Financial | attached | balanced | benchmark price | Calgary Monthly Housing Summary | Calgary Real Estate | Calgary Real Estate News | Calgary Real Estate News | Community | Conference Board of Canada | CREB® Chief Economist Ann-Marie Lurie | CREB® president Cliff Stevenson | detached | neighbourhood | Todd Hirsch | YYCRE

Related Articles

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}